Foreign Income After Returning to India: RNOR, FA, Stocks

Check when foreign income, US stocks, accounts, and assets become taxable or reportable in India under RNOR/ROR and Schedule FA.

The first mistake is treating tax, holding, and repatriation as the same decision

People returning to India often ask one rushed question: what happens to my foreign income and assets now? That sounds sensible, but it bundles together three separate problems. First, what does Indian tax law say about the foreign income in your current residential-status lane? Second, can you continue to hold the foreign bank account, brokerage, pension, or property abroad? Third, even if you can keep it abroad, should you actually move some of it now because your India-side operating model needs it?

The official sources do not answer those as one combined issue. Income Tax India draws the tax line through residential status. RBI's clarification under section 6(4) of FEMA addresses the ability to continue holding eligible foreign assets built while you were resident outside India. RBI's foreign-currency account FAQ then opens a separate decision about whether an RFC account is useful once you do repatriate some of that money. The move stays cleaner when you solve those in that order.

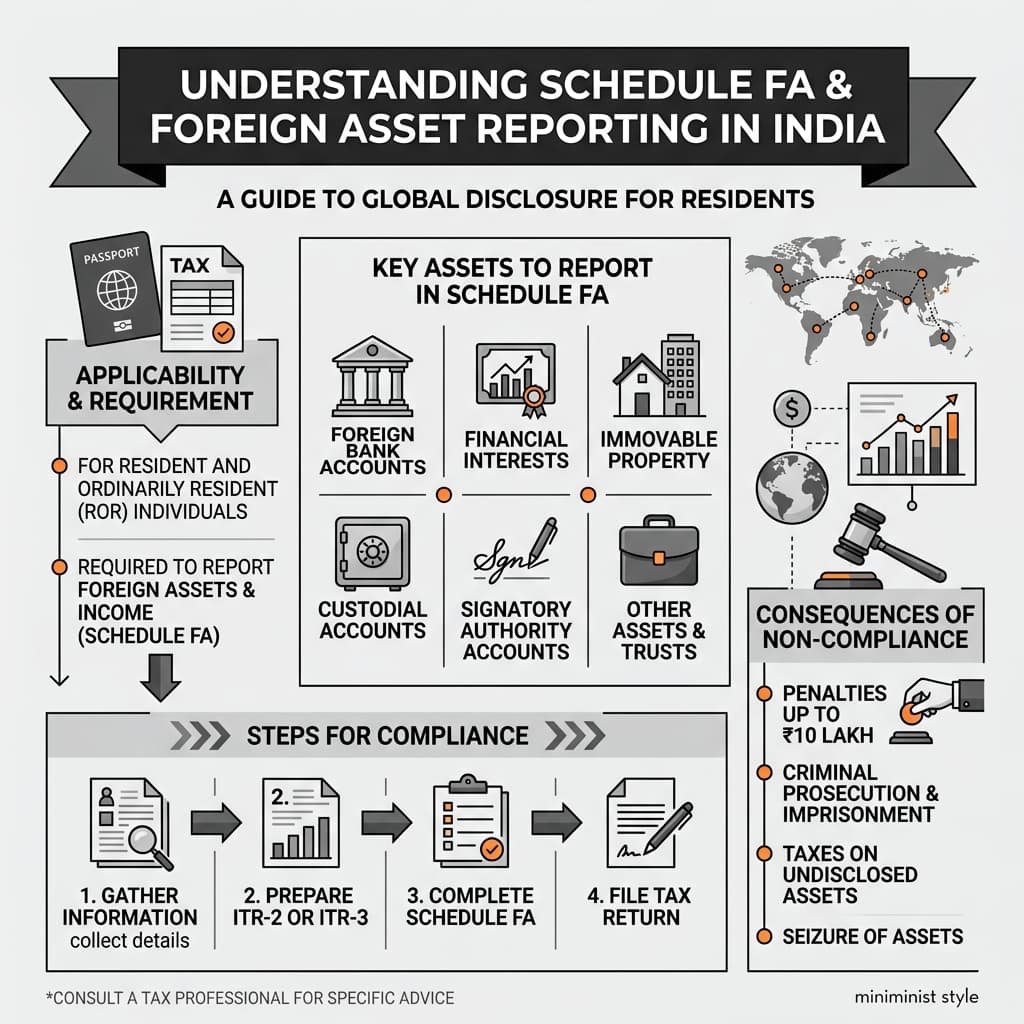

Schedule FA Reporting Framework

Foreign Asset Reporting & Holding Workflow

Start with the tax-status map before you touch the money

The highest-leverage distinction is still NR versus RNOR versus ROR. If you skip that, every later decision becomes noisy.

| Status lane | What India taxes by default | What people wrongly assume |

|---|---|---|

| Non-resident | Indian income, income received in India, and income deemed to accrue or arise in India. | That the move itself changes last year's tax result. It does not. The status is tested year by year. |

| RNOR | Indian income and, in general, foreign income only if it is derived from a business controlled in India or a profession set up in India. | That every kind of foreign income is automatically outside India tax forever. RNOR is a transition lane, not a permanent exemption. |

| ROR | Global income, including foreign income, becomes part of the tax picture unless relief applies under the law or treaty position. | That keeping the asset abroad prevents Indian tax from caring about it. Holding location and tax scope are not the same thing. |

Key steps before you close a foreign account or wire a large balance

Lock your likely status for the current and next Indian financial year

If you may be RNOR for a transition period, that fact changes how you should interpret foreign salary, dividends, pension, and bank-interest assumptions after return.

List each foreign asset by type rather than by country

Bank account, brokerage, pension, RSU proceeds, insurance, and real estate create different operating and reporting jobs even when they all sit in the same jurisdiction.

Separate the question 'can I keep it?' from 'should I move it now?'

RBI's section 6(4) clarification matters because legal ability to keep an asset abroad does not mean that all of it should stay abroad for your actual cash-flow plan.

Decide whether India needs rupee liquidity, foreign-currency continuity, or both

That determines whether you do nothing for now, repatriate to an India-side account, or intentionally open an RFC lane for money you want to keep in foreign currency after return.

Only then prepare the tax and reporting file

Do not leave acquisition records, statements, pension letters, and filing support until return season. The paperwork is easier while the foreign institutions are still familiar and responsive.

Need help with Tax & Residency?

Share your blocker in one line. Our experts will reply with practical next steps.

What section 6(4) changes in practice

RBI's clarification is important because returning to India does not automatically force you to liquidate or repatriate eligible foreign currency, foreign securities, or immovable property that you lawfully acquired while you were resident outside India. The smarter question is what amount India actually needs now and what amount is better left alone until your operating model is clearer.

Keep abroad, repatriate now, or use RFC: the decision frame

| Choice | When it fits | What it solves | What usually goes wrong |

|---|---|---|---|

| Keep the asset abroad for now | When the asset was lawfully built while non-resident and there is no immediate India-side need to convert or consolidate it. | Preserves flexibility while your first return years and currency decisions settle. | People bring everything back just because the move happened, then regret locking themselves into a rushed conversion or account structure. |

| Repatriate part of it to India now | When the money is genuinely needed for landing liquidity, rent, school fees, or the first year of domestic expenses. | Aligns money movement with the actual spending job rather than with emotion or internet noise. | People optimize fees before deciding which India-side account should actually receive the money after their status changes. |

| Use an RFC account intentionally | When you want a resident India-based account that can continue holding eligible foreign currency such as overseas pension benefits, balances realized from section 6(4) assets, or redesignated NRE and FCNR(B) balances. | Creates an India-resident operating lane without forcing immediate conversion into rupees. | People treat RFC as a universal answer when the real issue is still unresolved tax timing or poor India-side cash planning. |

The documentation pack to preserve before your first India filing season

The reporting burden is usually easier to handle when you prepare the file before foreign institutions start closing access channels or changing your status.

- Year-end statements for foreign bank accounts, brokerages, pension plans, and other financial accounts.

- Records showing when and how major foreign assets were acquired, especially if they were built while you were non-resident.

- Foreign tax documents and withholding statements that help you understand what was already taxed abroad.

- Employer or pension letters showing the nature of foreign payments, including superannuation or other post-employment benefits.

- A simple asset register for yourself: account name, jurisdiction, owner, current purpose, whether India needs the funds now, and whether the holding is expected to continue.

- Notes on any joint holders, signing authority, or legacy phone numbers still needed for account access and OTPs.

Need help with Tax & Residency?

Share your blocker in one line. Our experts will reply with practical next steps.

Where Schedule FA and return reporting enter the picture

Income Tax India's return guidance is a useful reminder that foreign-asset reporting should not be treated as an afterthought. The return helper notes that residents who held foreign assets, had signing authority in a foreign account, or earned foreign income during the year may need to furnish Schedule FA in the applicable return forms. That is a filing consequence, not a reason to panic or to move everything immediately.

The practical lesson is that once you are in a resident filing lane, your foreign footprint needs to be documented cleanly. A weak file creates avoidable confusion around whether an account was still active, whether an asset was built while you were non-resident, and whether a foreign-income item belongs in the current year at all.

RNOR is a transition lane, not a permission slip to stop planning

The expensive mistake is hearing that RNOR exists and then assuming every foreign-income and foreign-asset question can be postponed. RNOR helps only when you use the transition period to decide what stays abroad, what moves, what gets redesignated, and how the future ROR years will work.

Need help with Tax & Residency?

Share your blocker in one line. Our experts will reply with practical next steps.

Animated decision map

Interactive checkpoint

Turn this guide into a decision file

0 of 4 checked

Can I keep my foreign bank account or brokerage after returning to India?

Potentially yes, if the foreign assets were lawfully acquired while you were resident outside India. RBI's section 6(4) clarification is the key source here. The real follow-up questions are how the income from those assets is taxed in your status lane and whether India needs the funds now.

Do I have to bring all my foreign savings to India as soon as I return?

No. Returning to India does not by itself mean every foreign asset must be liquidated or repatriated immediately. The better approach is to move only the amount your India-side plan actually needs and make the rest a conscious hold-versus-move decision.

Does RNOR mean foreign income is never taxed in India?

No. RNOR changes the scope of taxation, but it is not a forever status and it does not make every foreign-income situation automatically exempt. You still need to classify the income correctly and understand when the transition ends.

When does an RFC account make sense after returning to India?

Usually when you want a resident India-based foreign-currency lane for eligible balances such as overseas pension receipts, money realized from section 6(4) assets, or redesignated NRE and FCNR(B) balances. It is strongest when it solves a real operating need, not when it is opened just because it sounds sophisticated.

Your tax year is already running.

RNOR status, exit timing, and DTAA benefits all depend on decisions you make before you land. Don't guess.